With the raising interest of selling goods online, the European market of alcohol sales via e-commerce has grown exponentially during the past years. Nevertheless, there are still a few obstacles for some of the businesses to expand to new markets, one of them being the compliance with different indirect taxes around the EU. With this article, Eurotax will briefly introduce the main concepts of excise duties for online alcoholic retailers in europe.

Excise duty definition:

Excise duty is a tax that is imposed by the government on certain goods produced, manufactured or imported within a country. It is typically applied to goods such as alcohol, tobacco, gasoline, and other products that are luxury or non-essential items. The purpose of an excise duty is to generate revenue for the government and to discourage the consumption of certain goods, as the increased price may make them less attractive to consumers. The tax is usually included in the price of the product and is collected by the manufacturer or seller, who is responsible for remitting it to the government. The rate of excise duty may vary depending on the type of product and its intended use.

General explanation regarding the scope of the Excise Duty Directive in Europe:

What are the matters covered by this Directive?

These rules cover, for example:

- the categories of products to which Member States must apply excise duties;

- the principles for determining who receives the revenue from excise duties;

- the rules applicable to the production, storage, and movement of products subject to excise duty.

Production and storage of excise goods:

Excise goods must be produced in tax warehouses. They can also be stored there when they are subject to duty suspension. Tax warehouses must be authorized by the national authorities, in accordance with the principles defined by the Union. These principles are set out in recommendation 2000/789/CEFR.

To be noted that excise duties are due as soon as these products are released for consumption.

How to apply Excise duty on your trade?

In the case of sales transactions, excise duties are generally paid in the Member State of consumption.

There are two possibilities to carry your goods as a company:

- You can keep your goods under duty suspension status – which means, the goods will not be subject to excise duties for as long as they stay under this status, and excise duties will only need to be paid once the goods are released for consumption.

- You can release your goods for consumption and ship afterwards – in such case, the excise duties will already be paid, and you will be able to sell your goods all around the country where it is cleared, or ship to other countries, where excise duties will become due.

If sales consignments have already been released for consumption (and therefore excise duty has been paid) in one Member State and are then transported to another one as its last destination, a refund system is set up to avoid double taxation.

How does it work for online alcohol retailers?

For distance sales B2C (sales to a private person in another Member State), the principle of taxation in the Member State of destination applies. First, the goods can only be shipped to private individual cross borders once duties are paid in the Member State of departure. Afterwards, excise duties must be paid in the Member State of destination for products, upon their arrival to the final recipient. As private individuals will never have an excise duty identification, it is always the vendor (or in some cases other liable party, such as fiscal representative) who must pay the excise duty.

To avoid double taxation, Directive 2008/118/EC provides a system of refund for excise duties paid in the Member State of departure. The refund conditions are settled by this Member State.

Accompanying documentation for distance sales (e-commerce) of excisable goods

As a seller, you must also establish a sales document for each shipment. This document must contain the different information about the company, type of products and quantity, with other information about your tax representative.

This document must accompany each of your shipments. It must therefore be affixed to the outside of the package or be inside. In the event of non-compliance with this obligation, the goods risk being confiscated by customs and the excise duties claimed from the recipient.

The implemented changes for alcohol excise duties as of 13th February 2023

Since February 13th, 2023, a new Directive has come in force, regulating the excise duties in the EU: Directive (EU) 2020/262FR. It replaces the old Council Directive 2008/118/ECEN , which lays down common provisions applicable to all goods subject to excise duty under EU law. This reviewed directive contains several measures aimed at streamlining and simplifying the processes for interactions between imports and exports and intra-EU movements of excise goods. It aims to approximate excise and customs procedures at EU level to improve the free movement of excise goods released for consumption in the single market, while ensuring that the correct tax is levied by the Member States.

Digitalization of Excise Duty reporting

The aim of the new excise duty rules following the update of the Directive on general arrangements for excise duty, is to move to digitalized and immediate information exchange on the movement of products subject to excise duties across the Union which will help authorities fight excise duty fraud.

At the same time, the new electronic system will simplify life for traders, especially smaller producers of alcohol, and will help them scale their sales quickly. To know that digital excise duty procedures were previously available only to traders operating under the so-called ‘duty suspension’ procedure. Until now, goods needed to be accompanied by physical hard copy paper declarations when the excise duty was being immediately accounted for at their destination.

Under the new measures all traders moving excise goods from one Member State to another in the EU will only need to submit digital transaction information into the already existing EU Excise Movement and Control System (EMCS).

The updated Directive on general arrangements for excise duty sets out general arrangements for goods subject to excise duty, including those around production, storage and movement of excise goods across the territory of the EU.

However, it seems that with the revised Directive, all excise duty transactions in the EU have become fully electronic as of 13 February 2023, except for the distant sales selling scheme.

Changes for the distance sales as of 13th February 2023

In the scope of the new Directive, it seems that the setup of excise duty reporting for distance sellers did not face significant changes. The main concepts that have changed are the following:

- The responsibility to declare excise duties will now lay with the ‘consignee’ instead of the ‘seller’. Therefore, should you run a business in logistics or have a marketplace without becoming the owner of the goods, it is a good idea to double check your liability for excise duty matters. Do not hesitate to contact Eurotax for further investigation into your specific case.

- Maintaining tax representation in distance sales (e-commerce): the Directive still allows the appointment of a tax representative to support professionals with their formalities related to their activity, to guarantee the payment of excise duties, but also to keep accounts of the product deliveries. As Eurotax is dealing with different Customs Authorities on a daily basis for more than 5 years, our team of experts will gladly assist your company in order to reduce the burden of compliance around the EU. Eurotax helps you with the management and payment of alcohol excise duties in several EU countries.

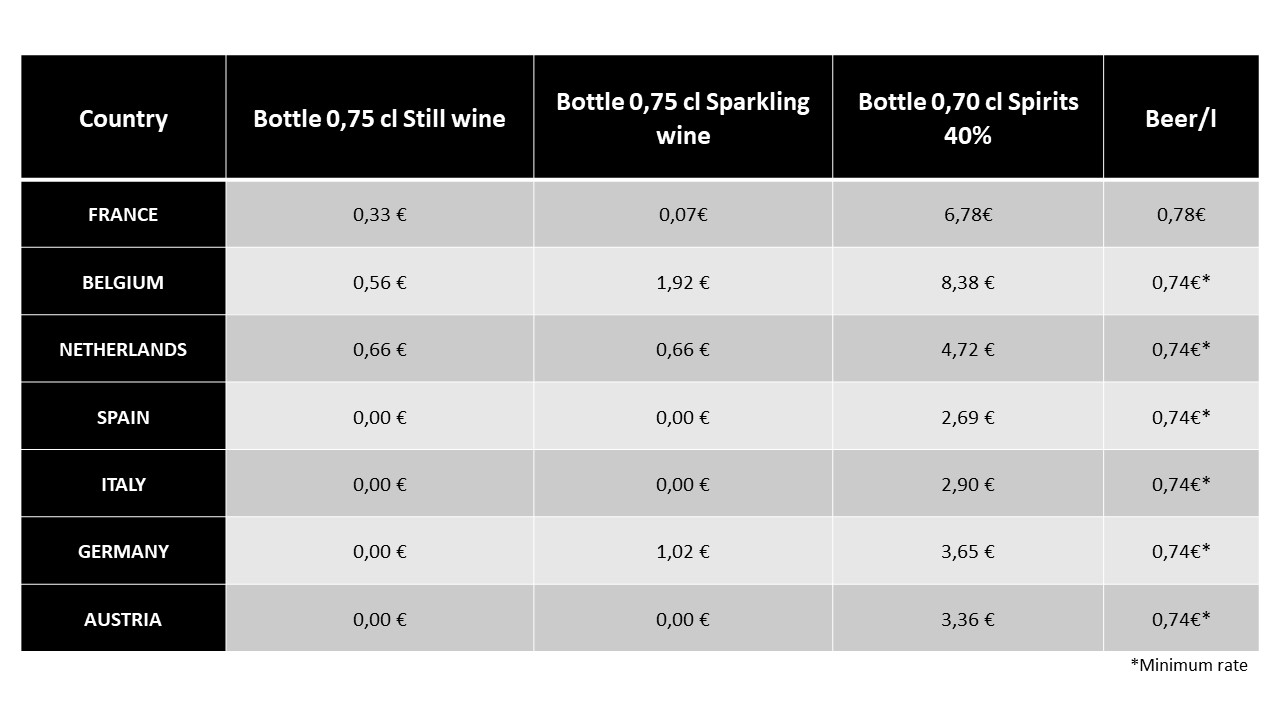

Alcohol excise duties rates in the EU

PS: These rates are subject to change, if you need more specific information do not hesitate to contact Eurotax.

With this range of measures on excise duties, the Directive is supporting a closer Single Market by digitalizing declarations, reducing the administrative burden to excise operators, and further preventing tax fraud. Contact Eurotax Team today to find out how to best take care of your excise duty formalities!

About the authors

Ikram Houti is a digital marketing manager at Eurotax, a company which offers different services to companies for VAT matters, customs & excise duties. Ikram regularly writes articles about indirect taxes, VAT & alcohol excise duties, she has several experiences in different companies where she deepened her knowledge about digital marketing, market analysis, finance and business strategies.

Ikram Houti is a digital marketing manager at Eurotax, a company which offers different services to companies for VAT matters, customs & excise duties. Ikram regularly writes articles about indirect taxes, VAT & alcohol excise duties, she has several experiences in different companies where she deepened her knowledge about digital marketing, market analysis, finance and business strategies.

Inga Baranauskaite is an indirect tax specialist with over 7 years of experience in the field. Inga has worked in different advisory firms on VAT and excise duty related matters, where she handled with both compliance and consultancy tasks. At Eurotax, Inga is currently responsible for business development and customer onboarding, taking care of developing and maintaining new services and partnerships, bringing the best value for Eurotax customers.

Inga Baranauskaite is an indirect tax specialist with over 7 years of experience in the field. Inga has worked in different advisory firms on VAT and excise duty related matters, where she handled with both compliance and consultancy tasks. At Eurotax, Inga is currently responsible for business development and customer onboarding, taking care of developing and maintaining new services and partnerships, bringing the best value for Eurotax customers.

More interesting articles for you:

Textile EPR in the Netherlands – Changes in 2023

Anti-Greenwashing Law: What does the EU Green Claims Regulation mean for brands in Europe?